Personalised support for your real estate project

You don’t need a genie’s lamp to finance your home! Looking to finance your home in Luxembourg with a mortgage? Our experts can offer you a mortgage tailored to your budget and goals. Discover our full range of real estate loans and mortgage rates.

Make an appointment at one of our property valuation centres

Explore all the benefits of a BGL BNP Paribas climate loan! Find out more about government subsidies.

By trusting BGL BNP Paribas’ real estate experts, you’ll give yourself the best chance to make your dreams come true.

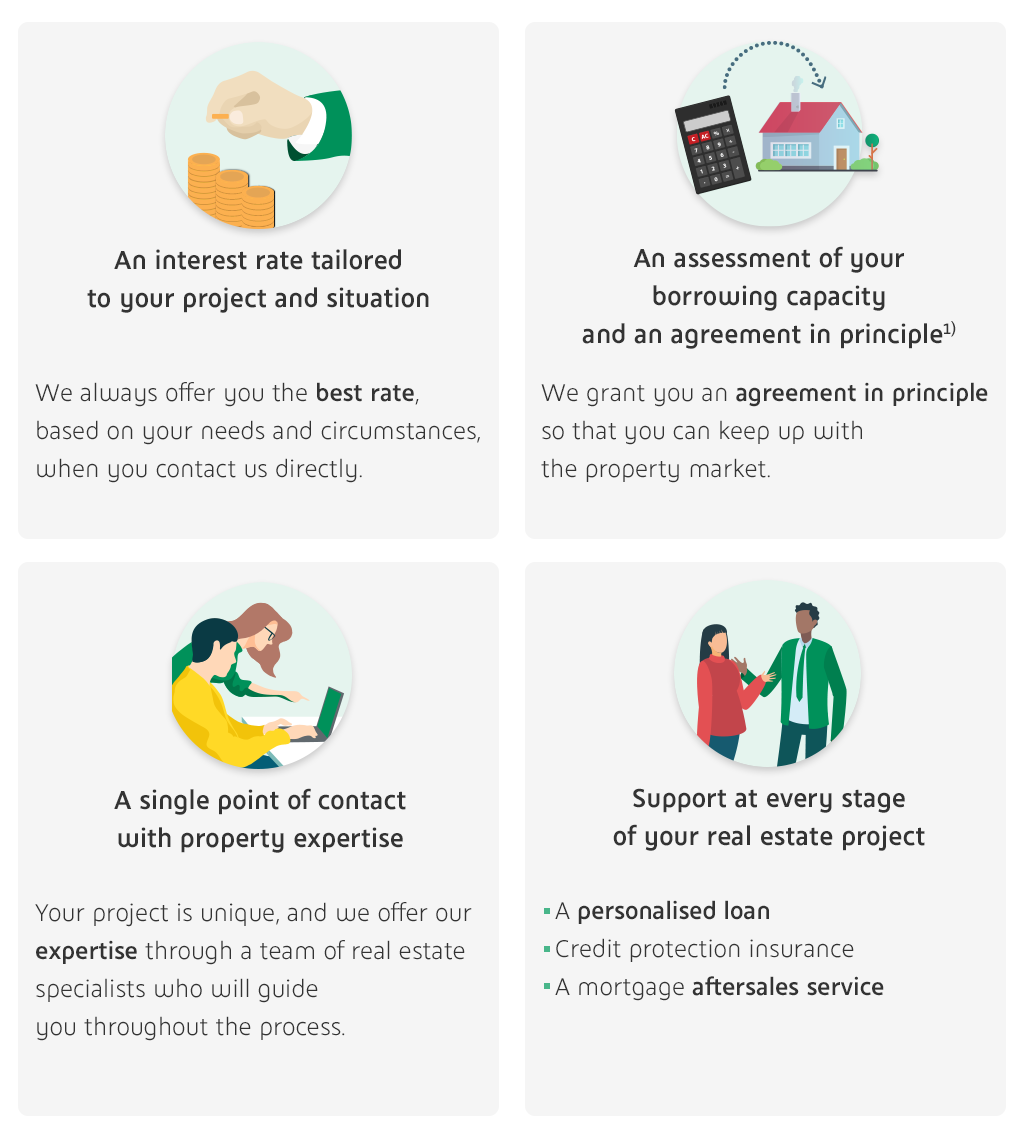

Our specialists are there to help you find the perfect structure for your loan, in line with your plans as well as your personal and financial situation.

Emma and Arthur want to buy their first apartment. Before starting their property search, they decide to asses their borrowing capacity online. During their search, they use the mortgage simulator to calculate their repayments. Having found their dream home, they contact their advisor to get a tailored solution.

Already a client? See the Loan on your Web Banking page to find out your borrowing capacity. You can apply for a home loan online once you have a specific project. 100% secure.

A home loan can be used to finance a property in Luxembourg and the Greater Region.

Key features:

How to apply for a loan online via the Web Banking app:

Quick and easy, in a few simple steps. Find out more.

For more complex projects, including bridging loans, please contact your adviser.

Make an appointment with your bank advisor to assess your financial position. Your income, savings and personal situation will determine your borrowing capacity.

The response time depends on the urgency and complexity of your project. We’ll do our very best to stick to your schedule.

The loan can be repaid early at any time. Fees apply under cerain conditions. If you’ve chosen a fixed rate loan, you may be required to pay break fees (early repayment penalties). The variable rate provides greater repayment flexibility.

Yes, you can take out a mortgage together without being married.

The state grants capital or interest assistance to adult individuals who take out a loan for the purpose of purchasing, renovating, converting or building. This can be for an apartment, land or a house. Certain conditions must be met in order to receive this assistance, in particular relating to income and the property’s surface area.

The state has also set up green loan options. These grant access to preferential loan terms for home energy retrofits.

Debit interest on mortgages is tax deductible. Various caps are applied depending on the purpose of the loan:

Tax deductibility varies based on the personal situation of each client and is subject to change.

You must be 18 or over to benefit from a home savings scheme. Then, in terms of tax deductions, households with one member aged 40 or younger will see their tax deduction limit doubled.

(1) Subject to approval of your application by the bank.